Market Snapshot | February 2026

By Nancy Curtin

Markets and Investments

Published October 10, 2023

As a follow-up to our recent article titled Climate Risk is an Investment Risk, we are highlighting the wide range of climate-related investment opportunities available to AlTi Tiedemann Global’s client base, subject to suitability and investor qualification. While some AlTi clients have been investing in climate opportunities for years, given the evolving market dynamics we are encouraging more of our clients to consider doing the same. We believe the addressable market for disruption of legacy energy systems and industry is massive, and the tailwinds from technological advances, changing consumer preferences, corporate commitments, and public policy have created an attractive backdrop for investing in this space.

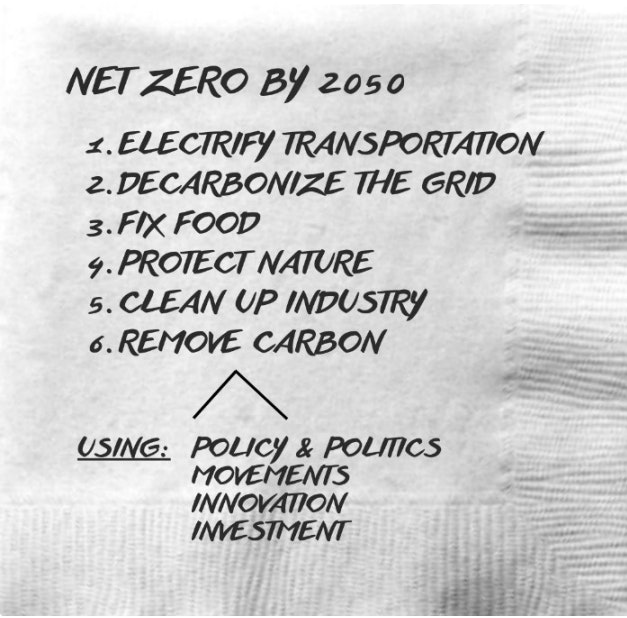

Legendary venture capitalist and author John Doerr of Kleiner Perkins described the requirements for a Net Zero economy on a napkin. These six areas could be recategorized in several ways, but in general, they represent the opportunity set for investing in the net zero future. Many research organizations and think tanks publish astronomical estimates of the capital needed to decarbonize the economy. Instead of focusing on those figures, we want to focus on a few climate opportunities where capital is focused on better solutions (cheaper, faster, cleaner) to existing problems within segments of the global economy.

Diverse set of opportunities: Investing in climate solutions is far from limited to a single asset class or a single sector of the economy. Depending on risk appetite, return objectives, and liquidity preferences, clients can participate in a range of investments. We believe investing in climate solutions can deliver portfolio benefits such as high (and often tax advantaged) cash flows, inflation protection, low correlation to traditional assets, and growth driven by the urgent need to decarbonize sectors such as industrial manufacturing, energy production, agriculture, transportation, and the built environment.

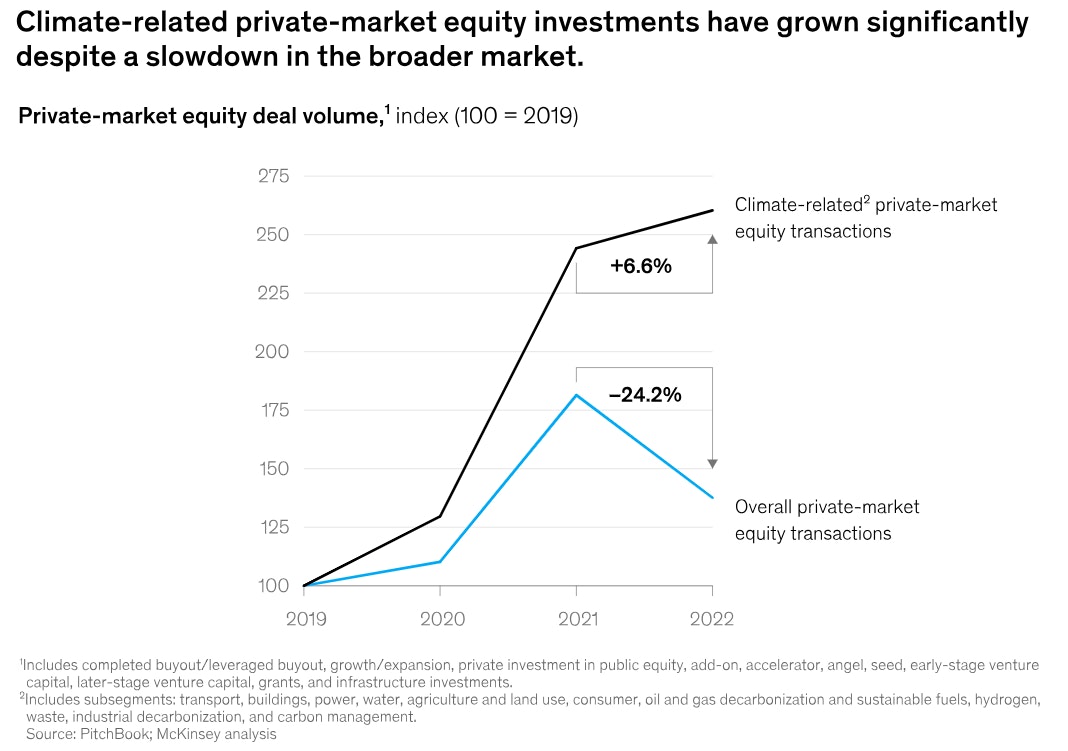

Increasing Investor Interest: Capital markets are beginning to take notice of this opportunity. Per McKinsey, “Climate-related private-market investment far outpaced the broader market in 2022 as measured by deal activity, the amount of capital deployed, and capital flows into dedicated funds.1

We believe there is significant synergy between intersecting segments of markets which are all needed for decarbonizing the global economy. For example, new technologies emerging from the world of venture capital need traditional decarbonization-focused private equity to reach a critical scale. New technologies improve the efficiency of renewable energy infrastructure while lowering costs and broadening the market opportunity. Venture capital backed companies can also improve the efficacy of nature-based solutions such as sustainable forestry and agriculture.

We want to highlight some of the opportunities which we find most compelling.

Renewable Energy Infrastructure - We believe that well-structured investments in renewable energy infrastructure present great opportunities for strong risk adjusted returns. Technologies such as wind, utility scale solar, and community solar are now well-established and commercially attractive due to cost curves which have fallen sharply over the past twenty years. Many governments are still in the very early stages of adding these assets to their power generation infrastructure, and we see rising demand driven by new public policy initiatives and corporate Net Zero commitments. Once in production, these renewable energy assets typically derive cash flows from 20+ year fixed rate contracts facing investment grade counterparties. These assets can deliver high rates of current income and tax advantages in early years due to accelerated depreciation. We continue to see technological innovation in this space giving rise to cost and efficiency reductions. As more corporations and state, and local governments set emissions reduction targets, the strategic value of these assets should rise, creating opportunity for capital appreciation.

Intermittency is one of the challenges with wind and solar, but help is on the way through public policy initiatives such as the IRA and advances in areas such as battery chemistry. Energy storage systems (batteries), either traditional lithium batteries or more novel technologies, are key to managing intermittency, and represent a significant growth opportunity. For example, Form Energy is building multi-day grid scale energy storage systems from iron ore, while Rondo Energy and Antora Energy are building thermal batteries to help decarbonize the power grid and high heat industrial processes. We believe deployment of these types of technologies alongside solar and wind power generation assets will become part of a combined solution to reliably replace legacy fossil-based power generation infrastructure. This presents a significant opportunity for investors in renewable energy infrastructure.

Sustainable Forestry – We believe that sustainable forestry presents a proven and uncorrelated opportunity for investors that new markets and technologies are making even more attractive. The long-term orientation of timberland investments is well aligned with endowment style investors who seek to protect and maintain wealth across generations. In addition to cash flows from timber harvests, sustainable forestry can generate returns from conservation easements, recreational leases, and the appreciation of the underlying land value over time. These factors make forestry a strong inflation hedge that, when properly structured, is also tax efficient. From 1987-2022, the average rate of return of direct timber investments on the NCREIF Timberland Index was 10.3%. For comparison, the S&P 500 returned 10.4% and MSCI All Country World Index returned 10.4% over the same period, but with significantly higher drawdowns and more volatility than forestry.2

The carbon sequestration potential of well-managed forests provides further upside as carbon markets develop and net-zero commitments create demand for high-quality carbon credits. Venture-stage companies like Funga and Living Carbon are deploying new technologies that accelerate tree growth which could further improve sustainable forestry returns over time. While the traditional portfolio diversification benefits are enough to recommend sustainable forestry alone, market and technological advancements are making it an even more attractive opportunity.

Decarbonization-Focused Private Equity - We believe that private equity can play a prominent role in decarbonization by providing capital and strategic advice to companies seeking a new growth path in a decarbonizing world. We’ve seen firms prove out this model by partnering with operators and acquiring real asset and infrastructure projects with a path to decarbonization. The premise here is that sustainable real assets using renewable inputs are fundamentally more efficient and economical than conventional real assets. Examples from our platform include companies electrifying fleets of school buses, EV charging stations for the trucking industry, renewable deployment using existing interconnection infrastructure, and developers of energy efficient solutions such as cookstoves and methane leakage systems. Private equity can also play an important role here to aid in the deployment of new technology delivered through infrastructure services to end customers. It has been a challenge for large institutions (municipalities and corporations with decarbonization targets) to work with less established technology providers. Finally, many established traditional private equity investors are beginning to focus on decarbonization as a prominent value driver for their portfolio companies. Agricultural waste-to-value operator Cycle0 is one example of a private equity backed company reducing landfill waste while displacing fossil based natural gas with carbon neutral renewable natural gas. If lower carbon products can be substituted for conventional products at an equal or lower cost (by recycling feedstocks or eliminating by products and waste, for example), companies can reduce production costs. This creates a competitive advantage with added tailwinds fueled by growing demand for green products. Private equity is especially suited to assist middle-market businesses in decarbonization as they grow because many of these businesses lack the internal resources to do it on their own.

Climate Technology Venture Capital – Venture capital aimed at solving the climate crisis is one of the most compelling market opportunities on our radar. Falling costs of computing power, adoption of artificial intelligence, better sensors, more accurate monitoring data, and advances in synthetic biology suggest a wave of innovation and disruption that will touch nearly every sector of the economy and accelerate decarbonization. These advances allow for faster company formation and faster iteration on an idea such that deep technology businesses can reach pilot stages faster than ever in history. As funding is reduced for much of the venture capital world, we see premier climate technologies remaining resilient. Recent examples of venture capital3 backed business raising large pools of expansion capital include circular battery supply chain operator Redwood Materials, novel lithium extraction operator Lilac Solutions, geothermal project developer Fervo Energy, and green steel manufacturer Boston Metal. We’ve seen a significant rush of technical talent move towards climate technology companies over the past two years as professionals decide they want their first or second career to be focused on this issue. In addition, significant dry powder remains available for companies at various stages of maturity (venture capital, growth equity, and private equity). In addition to investment capital, public programs (such as the IRA and Chips Act) provide incentives for development through loans and non-dilutive grants.

While climate opportunities have been in and out of favor by investors over their history, we believe we are at the beginning of a new phase for growth. The landscape has evolved over the years and our climate platform has evolved and grown. We’ve been working diligently to build relationships with successful investors and operators in this space over the past ten years, and we believe this will benefit the AlTi Tiedemann Global client base.

Sources:

1 McKinsey: Climate investing: Continuing breakout growth through uncertain times

2 NCREIF, Bloomberg

3 The following examples are in no way intended to be considered a recommendation or an offer to sell or a solicitation of any offer to buy and are not open for public investment.

Notes & Important Disclosures

This information is being provided by AlTi Global, Inc. (“AlTi”), exclusively for use by recipient. For the purposes of this disclosure, AlTi includes certain of AlTi’s affiliates that are registered as investment advisers with the U.S. Securities and Exchange Commission, (each, an “AlTi Affiliate RIA” and collectively, “AlTi Affiliate RIAs”) that provide investment advisory services. Any investment products referred to herein are managed and / or advised by one or more of AlTi Affiliate RIAs. No part of this material may, without AlTi’s prior written consent, be copied, photocopied, or duplicated in any form, by any means. AlTi is providing this information solely in connection with providing general investment advisory services and is not in connection offering investment advisory services with respect to any “private funds” that are managed by such AlTi Affiliate RIAs. The information provided is in no way intended to be considered a recommendation, or an offer to sell, or a solicitation of any offer to buy, an interest in any security, by AlTi or any AlTi Affiliate RIA, including an interest in any investment vehicle or any other financial product, including any investment advisory, wealth planning or trust arrangement managed or advised by AlTi or any AlTi Affiliate RIA, nor does it constitute investment, legal, or tax advice with respect to the products and services and it is important that you do not rely on its content when making an investment decision. Neither AlTi nor any AlTi Affiliate RIA make any representations through this information as to whether any security or other financial product is suitable to you or will be profitable. This information is not intended as a formal research report and should not be relied upon as a basis for making an investment decision. You should obtain relevant and specific professional advice before making any decision to enter into an investment transaction. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investments are not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other governmental agency. Prospectuses and offering documents should be read thoroughly before investing. No representation is made that any client will or is likely to achieve its objectives, that the strategies, investment process or risk management referenced in the information provided will be successful, or that any client will, or is likely to, make any profit, or will not suffer losses, including loss of principal. Past performance is no guarantee of future results. Opinions regarding the suitability of investment approaches, including risk allocations and other portfolio decisions, are not tailored to any specific client, do not constitute recommendations, and are solely provided to facilitate discussion. Individual investor portfolios are constructed based on the individual’s financial resources, investment goals, risk tolerance, investment time horizon, tax situation and other relevant factors. Any statements, assertions or the like (collectively, “Statements”) regarding prior or future market or other events, or views about investing, are based upon AlTi’s beliefs, which may not reflect those of the firm as a whole, unless the information provided includes the source(s) with respect to such Statements. Additionally, AlTi Affiliate RIAs may pursue investment strategies for clients that do not reflect or contradict the beliefs set forth in any Statement at any time, including at the time of publication. The Statements involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond the control of AlTi. Future evidence and actual results could differ materially from those set forth in, contemplated by, or underlying these Statements, which reflect AlTi’s beliefs at the time of publication and are subject to change. In light of these risks and uncertainties, there can be no assurance that these statements will prove to be accurate in any way. Information given herein is believed to be reliable, but AlTi does not warrant to its completeness or accuracy, nor does AlTi assume any obligation to update or revise such information. Certain information has been provided by and/or is based on third-party sources and, although believed to be reliable, has not been independently verified and AlTi is not responsible for third-party errors.