Climate Risk is an Investment Risk

By Brad Harrison & Alex Hokanson

Climate Risk is an Investment Risk – The US Treasury Secretary’s Recent Comments You May Have Missed

US Treasury Secretary Janet Yellen recently had some stark comments for investors: “As climate change intensifies, natural disasters and warming temperatures can lead to declines in asset values that could cascade through the financial system. And a delayed and disorderly transition to a net-zero economy can lead to shocks to the financial system as well,” Secretary Yellen stated on March 7, 2023. Unfortunately, her comments on climate risk were quickly overshadowed by the Federal Reserve’s swift action to shore up the US banking system just days later. However, what she said at the first meeting of the Financial Stability Oversight Council (FSOC) Climate Related Risk Advisory Council in early March should be elevated in light of this fast-moving news cycle.

“As climate change intensifies, natural disasters and warming temperatures can lead to declines in asset values that could cascade through the financial system. And a delayed and disorderly transition to a net-zero economy can lead to shocks to the financial system as well.” Janet Yellen, US Treasury Secretary. March 7, 2023

At that meeting, Treasury Secretary and former Federal Reserve Chair Janet Yellen and her team didn’t pull any punches. The message was stark and clear: global climate related impacts including warming temperatures and natural disasters are likely to become an increasing threat to asset prices and the stability of the financial system. Seeing the collapse of several banks in real time, we’re all getting another reminder of the inter-connectedness of our financial system. Now let’s apply that to an even more globally connected and fragile system – the climate – and you’ll quickly recognize why de-risking portfolios to adapt to the changing climate and investing in the net zero transition opportunities makes economic sense.

Banking and insurance companies were called out during Yellen’s remarks because of their significant role in providing liquidity and ensuring appropriate risk transfer mechanisms. The report highlighted a five-fold increase in the economic cost of natural disasters since the 1980’s. Consider the recent hurricanes in the US, drought in Europe, and flooding in China, all this in the very early stages of what will be at least a 30-year period in which the carbon already in the atmosphere is raising global temperatures. These natural disasters and warming temperatures will be felt globally, often by populations without the financial resources for sufficient adaptation.

This is not meant to be one of those climate scare pieces, but rather meant to portray the implications of climate change on asset values and the global economy. “These impacts are not hypothetical. They are already playing out,” she continued. The frequency, severity, and unpredictability of extreme weather events are increasing. From 1970-2019, the number of annual extreme weather events has increased by a factor of five, according to data from the World Meteorological Organization (WMO). The cost of extreme weather events has increased nearly eight times globally – which equates to a cost per event increasing nearly 77%, inflation adjusted, over the past 50 years according to recent research from the WMO and Barclay’s Corporate and Investment Bank1. As one of the many results of these trends, insurance companies are pulling back from insuring property in at-risk areas such as low-lying coastal regionals and flood plains.

As the effects of climate change increases, the number of at-risk areas is expected to increase. This pull-back in insurability adversely impacts property values. Property is collateral for loans in the banking system. Reduction in collateral means lower recovery rates on loan losses and more stress on the banking system. Lower property value also reduces consumer spending through the wealth effect. “Developments like these can spill over to other parts of our interconnected financial system,” continued Yellen.

Considering this global inter-connectedness, more and more, companies that emit greenhouse gases are going to be held accountable and forced to pay for remediation in some form. “Taking climate change into account is prudent risk management,” Yellen continued in her remarks, “…as it is critical to improving the resilience of the U.S. financial system to the effects of climate change”. Reductions in insurability, reductions in credit availability, reductions in consumer spending, and significant remediation costs would affect the prices of nearly all assets. Most of the effects are bad. However, there are assets that may benefit from this disorder.

While we’re cognizant of the risks, we’re not shy to assert that climate change presents one of the most exciting investment opportunities of our lifetimes, and we believe our timing, access, partners, and the opportunity couldn’t be any better.

Capitalizing on the net zero transition

Investment management involves identification of risks and opportunities. One category of assets which may benefit from the disorder are companies which mitigate climate change by reducing greenhouse gas emissions or by sequestering carbon emissions. For simplicity, let’s just call these climate technology companies. We’ve recently seen them benefiting from rapid technological innovation and supported by the legislative process. The Inflation Reduction Act provides massive subsidies for domestic clean energy solutions such as solar and wind energy production, and for storage solutions through batteries and green hydrogen. That same legislation put forward significant fines for companies responsible for leakage of methane (a very potent greenhouse gas) into the atmosphere.

Despite promising progress in the composition of the global economy, achieving full decarbonization will require a huge amount of public and private investment. It’s estimated that $135 trillion of investment is needed by 2050 to decarbonize the global economy.2 The investments are supported by very considerable economic, policy, and technological tailwinds. National and corporate net-zero commitments, which comprise nearly 90% of global emissions, are clear indicators of market demand for new technologies.

And investors are taking notice. Climate technology venture capital saw record inflows in 2022, the same time that funding and valuations fell sharply for traditional venture backed SaaS and eCommerce businesses. According to recent insights from McKinsey and PitchBook, climate focused private equity and venture capital investments reached nearly $200 billion in 2022, up three times the amount invested just three years before – with those focused on power generation and the energy transition accounting for roughly half of this new investment3. Contrary to any worries about a bubble, our view is that we do not have nearly enough capital moving into the climate technology space. This is not “clean-tech 1.0” where mistakes were made, but a lot of lessons were learned.

Economic growth and emissions reductions are becoming mutually reinforcing trends

If climate scenarios turn out to be as bad as several thousand expert scientists believe it will be, you may want to help fund the solutions that will both build the Net Zero economy and generate strong financial returns. In doing so, you’d be joining the likes of some amazing decarbonization companies working on multi-day grid scale battery systems, nitrogen fixation from sunlight and water, sustainable mining of lithium, electric short haul aircrafts, as well as nature-based companies working on industrial biology, plastic eating enzymes, and plant-based proteins. We could go on and on.

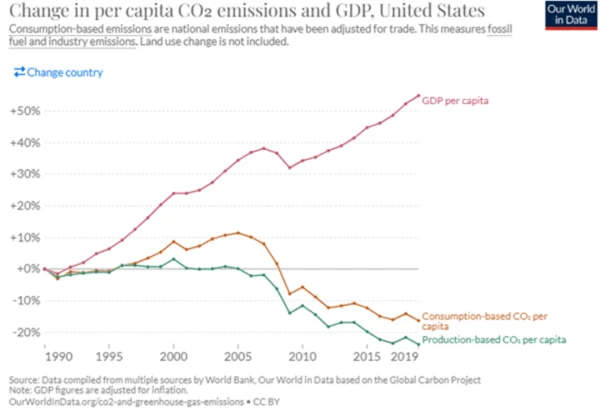

But before we do, let’s be clear. Our key point is that climate risk is investment risk. More than 91% of global GDP falls under net zero targets4. It used to be thought that we needed to decouple economic growth and rising carbon emissions. That’s no longer the case. Over the last twenty years, GDP per capita has risen substantially while CO2 emissions per capita has declined in several countries, including the US.5 Reducing emissions and achieving economic growth had previously been seen as conflicting goals. Now, emission reductions and economic growth are becoming mutually reinforcing trends.

Many of our clients have been investing in dedicated climate investments and the low-carbon future for a decade or more. We believe we have built enduring relationships with some of the top venture capital firms in the space, as well as later stage investors in growth equity, infrastructure, and buyout. We’ve done so because we think we can make strong market returns and – we hope – address some of these challenges.

About the Authors