Time to Consider Endowment-Style Investing

By Nancy Curtin

We believe we are entering a different investing environment than the one that characterized the past decade. The end of loose money, zero-bound interest rates and disinflation that led to strong gains, particularly for US stocks and bonds, may be replaced by an era of volatility and the outperformance of assets that have been ‘unloved’ by investors.

In addition, we believe that a simple 60/40 portfolio of stocks and bonds is unlikely to outperform a more diversified endowment-style portfolio, including an allocation to alternative investments, in this new investing regime of the future.

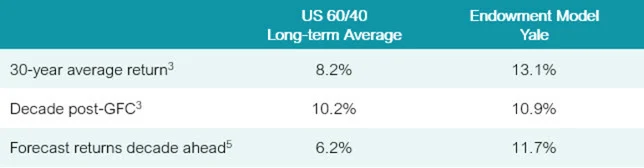

The US stock market dramatically outperformed most other asset classes in the decade after the Global Financial Crisis (GFC). From a low of 667 in March 2009 until the onset of Covid in 2020, the S&P 500 compounded at 16%, well ahead of its historic 10%1 100-year average gain and significantly greater than international equity markets and many forms of alternative investments. A 60/40 US-based passive stock/bond portfolio compounded at 10.6% over this period, surpassing its long-term average return of 8.2% and significantly higher than a 60/40 allocation that included non-US based stocks of 7.4%2.

It was a great time to invest in a 60/40 portfolio with a US market bias, but investors likely ‘over-earned’ during this period.

What ‘under-earned’ was endowment-style investing, an approach in which an investor takes advantage of the premium returns typically available in alternative investments such as private equity, private credit, real estate, hedge funds and real assets. Endowment-style investing was pioneered by the late David Swensen, who ran Yale’s endowment for more than three decades, and has been practiced by some of the largest and more sophisticated long-term investors. During Swenson’s tenure, Yale generated exceptional returns of 13.1% annually, outperforming a traditional US 60/40 stock bond portfolio by 4.9% per year3. Swenson’s Yale model also demonstrated the benefits of diversification, what is often known as ‘the only free lunch in finance investing’: not only did the strategy deliver above-average returns, but the Yale portfolio had lower volatility than comparable portfolios4.

However, Yale’s endowment returns in the decade following the GFC were significantly lower than their long-term average at 10.9%3 per year, a still respectable return roughly in-line with a US 60/40 portfolio. In other words, broad-based diversification into alternatives practiced by Yale (and others) delivered about the same return as a less complex, lower cost and more liquid US 60/40 allocation (+70bps3). Endowment-style investing in that sense ‘under-earned’ versus its long-term return over this period.

Markets in our view have a habit of reverting back to long-term trends. Long-term capital markets’ assumptions make forward adjustments for these over- and under-performances of asset classes, as well as for changes in interest rates and inflation.

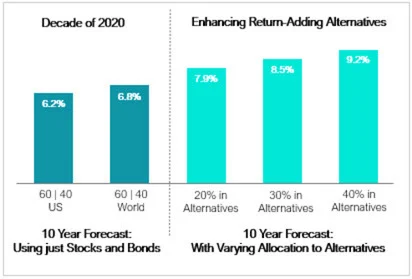

In the table below, we compare the opportunity set looking forward, based on capital markets assumptions of 10-year forecast returns. In general, returns overall are forecast to be lower given the rise in interest rates.

A pure 60/40 allocation, particularly one with a US dominant bias, is forecast to deliver around 6%5 in the decade ahead versus close to 12% for the endowment portfolio (based on Yale’s current asset allocation) that has both broader international equity and alternatives allocations.

Markets in our view have a habit of reverting back to long-term trends. Long-term capital markets’ assumptions make forward adjustments for these over- and under-performances of asset classes, as well as for changes in interest rates and inflation.

In the table below, we compare the opportunity set looking forward, based on capital markets assumptions of 10-year forecast returns. In general, returns overall are forecast to be lower given the rise in interest rates.

A pure 60/40 allocation, particularly one with a US dominant bias, is forecast to deliver around 6%5 in the decade ahead versus close to 12% for the endowment portfolio (based on Yale’s current asset allocation) that has both broader international equity and alternatives allocations.

Why do we believe this?

We believe the decade ahead will be different in a number of ways that should benefit investors with more broad-based diversification:

- After a decade of zero interest rates, excess money creation and disinflation, bond yields are repricing to more normal long-term levels. Fixed income, in both public and private markets, has already become more attractive than in the past decade and will likely become even more so. It will also likely be a greater source of both income and portfolio diversification, the latter as its correlation to other assets falls.

- Inflation rather than disinflation will likely remain a source of concern. While we believe that Central Banks will be successful in easing the abnormally high levels of inflation that we have experienced post-Covid, we think inflation could prove sticky in the 3%+ range. Secular forces such as onshoring of key supply chains, more of a ‘Beggar Thy Neighbor’ geopolitical environment, the costs of funding the energy transition, and underinvestment in key commodities are likely to conspire to keep inflation an ongoing concern in the decade ahead.

- Inflationary regimes have tended to favor different types of asset classes than disinflationary periods, with many of these asset classes trading at attractive valuations after underperforming over the past decade. We suspect that some unloved parts of the market such as international, value and small/mid-cap equities may surprise on the upside in terms of relative performance.

Moreover, alternative asset classes can potentially provide further upside return and increased diversification.

Private Equity

Private equity can provide access to long-term secular growth themes, many that cannot be accessed in public markets. The asset class has historically been able to deliver more than twice the return of public markets over a long-term timeframe7.

We continue to like disruptive and emerging technologies in automation and the green energy transition, the latter being an enormous imperative of government and investors in the years ahead. We believe top-tier managers who can use proactive value-adding strategies such as M&A, sector consolidation, investment in technology and cost rationalization may be able to drive strong profitability growth over the coming years.

Private markets, in our view, are also one of the most direct ways to access impact investments, where we have identified a range of dedicated managers and strategies poised to benefit from a world moving towards carbon neutrality and a more inclusive and equitable society.

Real estate and real assets

Real estate has fared well in past higher inflationary environments as investors flock to real assets with inflation protection. We particularly like exposure to real estate with long-term secular supply/demand imbalances such as housing, industrial and retail storage, industrial parks and last-mile e-commerce fulfilment.

Greening of real estate is also an important secular trend. We believe that buildings with lower carbon emissions, greater energy efficiency, and greener indoor and outdoor spaces will remain in high demand and can attract premium pricing. Quality locations with strong anchor tenants and built-in inflation stabilizers can be highly attractive from a return perspective and tax-advantaged for certain client jurisdictions.

For investors adverse to the illiquidity of long-term real estate investments, an allocation to real assets such as gold or commodity-based may be an appropriate complement to portfolios.

Hedge funds

We believe that the decade ahead will see significant increases in asset class volatility.

Managers who can benefit from rapid changes in market direction and have the ability to identify associated market inefficiencies should be able to provide interesting and alternative sources of return. Many hedge funds that struggled in the post-GFC decade due to low interest rates and low levels of volatility may well thrive in the environment ahead. We believe that exposure to a diversified range of absolute return managers who can take advantage of more volatile market conditions and pricing inefficiencies could add to consistency of returns and dampen overall volatility.

Importantly, alternatives allow investors to gain exposure not only to enhanced returns, but also to diversified sources of return. The more one can diversify a portfolio, the greater the reduction in risk8. Thus, by adding an allocation to these types of alternative asset classes, these more diversified portfolios may be able to deliver both higher returns and lower risk9 versus a classic 60/40 portfolio.

Sounds like nirvana?

Financial markets are never a certain bet and investing in alternatives also comes with its own set of risks. Alternatives are less liquid and, in the case of private equity, illiquid for many years; they are also less transparent and more complex.

Yale and other endowments accept these risks in the context of their long-term time horizon. This gives them an advantage in investing as they can allocate capital to these potentially higher-returning parts of the market, to garner higher overall returns while reducing portfolio risk through diversification.

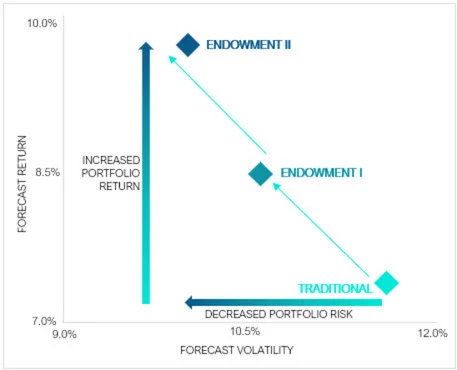

This concept is illustrated in the chart below, with reduced allocations to alternatives, more consistent with the needs of long-term individual investors.

The chart compares the assumed forecast return and volatility10 for a traditional 60/40 portfolio versus a portfolio inclusive of a 20% allocation to alternatives (called Endowment I) and one with a 40% allocation to alternatives (called Endowment II). The alternatives allocation is based on exposure to private equity, real estate and hedge funds, in varying proportions.

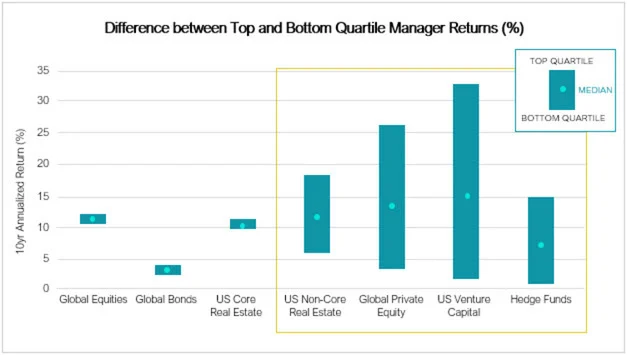

But the real value-add in an alternatives allocation is that these asset classes are more inefficient, where manager selection skill and access are critical. Notably, the distribution of returns between the top- and bottom-quartile alternative asset managers in alternatives is much wider than for those in public markets10. This makes having access to the best-performing managers in alternatives one of the secrets to these enhanced returns and long-term endowment-style investing success.

This dispersion in return is demonstrated in the chart below.

What does this mean for AlTi and our clients?

- As a global firm with more than 50 investment professionals and long-standing expertize in alternative investing, AlTi has the capability to build customized portfolios that meet client needs. Allocations to liquid and less-liquid alternatives can be built to incorporate the needs and goals of each client as appropriate.

- We can offer endowment-style portfolios that align to risk, return, liquidity goals and impact orientation.

- AlTi can provide access to top-performing managers across alternative assets that have consistently been able to deliver top-quartile returns.

About the Author