Quarterly Market Update and Outlook | October 2023

By Nancy Curtin

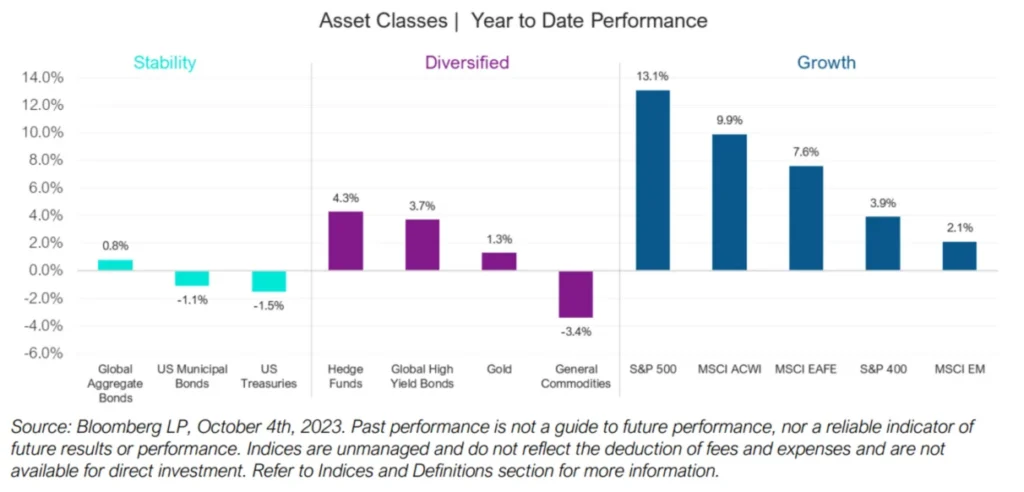

Markets: After a strong start to the year, stock and bond market returns have corrected.

Stability: Longer-dated government bond yields have risen, largely driving returns into negative territory.

Diversified: Hedge funds, high-yield bonds (credit) and gold remain important diversifiers and are still positive year to date. The rise in oil prices has led commodity returns to be less negative.

Growth: Stock markets have corrected from peak levels in July. Expectations of slowing GDP are weighing on growth assets, though markets (particularly US) still have positive YTD gains. Being diversified with exposure to growth, value and energy infrastructure has helped our portfolios mitigate some of the downturn.

The catalyst for a correction in markets has been a combination of factors:

- Rising longer-dated government bond yields. The rise in US government bond yields by almost 1% since June is a significant tightening of financial conditions. The rise in yields is partly a function of investors demanding a higher return on government debt, given the size of the US fiscal deficit and concerns around increased Treasury issuance. Higher long-term yields raise the cost of capital for all borrowers and increase risks of instability in leveraged areas of the economy.

- Rising oil prices. Recent increases in the price of oil by 30% serve as a tax on the consumer through higher retail gas prices. Persistent higher oil prices could impact inflation expectations, sparking a possible second wave of inflation. Notwithstanding the current tragic conflict in Israel, we think that oil prices will settle lower as Saudi removes their production cuts (expected by the end of this year) and as slowing global growth reduces demand.

- Rising US dollar. The strong US dollar is a form of global tightening as assets move back to the US and import prices in international markets become more expensive. This comes at a time of vulnerability in Europe and China, which have already been slowing.

Markets will remain volatile as investors assess the impact of these risks on global growth and future earnings. However, tightening in financial conditions has a silver lining as this might be what is needed to quell inflation. In the words of Mary Daly, San Francisco Federal Reserve Bank president: “Recent tighter credit conditions could help the Fed by bringing inflation down, even without additional policy adjustments.”

Fundamentals: The US economy has remained resilient and now needs to slow.

The tightening of financial conditions comes at a time when the US economy has remained surprisingly resilient. In contrast to Europe and China, the US experienced an acceleration of growth in the third quarter – perhaps a function of summer-seasonal travel or back-to-school spending. Consumption (which makes up ~70% of GDP) is forecasted to rise 4% in Q3, up from 0.8% in the second quarter. This comes despite 11 interest-rate hikes and the highest overall interest rates in 22 years.

Larry Summers calls the US an “Energizer Bunny Economy”, with job growth accelerating in the face of tighter credit conditions. Indeed, recent jobs data expanded by almost double what economists had expected. Core inflation and wage growth around the 4% mark continue to be too high for the Fed, although both measures are moving in the right direction.

There are several reasons that the US economy has remained so resilient.

- Consumer confidence: US households accumulated excess savings during the pandemic that they are now spending on all forms of experiences, boosting the service economy. While these savings are dwindling (estimated around $200bn versus $2trn at the peak in 2022), overall household net worth has increased due to gains in property prices (now back to pre-pandemic levels), year to date gains from the US stock market and consumers’ ability to earn elevated returns on cash. The strong jobs market and wage gains have also contributed to consumer confidence.

- Less interest-rate sensitivity: households and businesses locked in low borrowing costs so have been less sensitive to rising interest rates. For example, 75% of US mortgage holders carry 30-year fixed mortgages with rates below 4%. Large cap companies have seen net interest payments decline, even as the Fed has raised rates due to lower borrowing costs on debt refinanced in 2021. The refinancing of this debt is not a risk until 2026 at the earliest.

- Stimulative fiscal policies: just as the Fed has been raising rates, the US government has supported growth with more than $1.5trn of multi-year fiscal programs. Companies have taken advantage of incentives and subsidies from these programs, with an estimated $200bn in projects commenced this year. Government spending has accelerated corporate investment spending. Investment rose at a rate of 7.4% in Q2 and is now at the highest level of GDP since the late 1980s. Continued investment spending improves productivity. Indeed, the US recorded its biggest increase in productivity in almost three years at 3.5% in Q2 from 1.2% in Q1.

- Onshoring beginning to work: the US trade deficit also narrowed in August, its lowest level since September 2020, due to the continued weakness of imports as signs of onshoring take hold. This puts net trade on track to contribute to GDP growth in Q3.

In terms of GDP components, consumption (C), investment (I), government spending (G) and trade (X-M) in the US are all contributing to economic growth, despite the high interest rates. At the same time, C, I, and G are either negative or neutral in Europe and China. This dichotomy is what is causing US dollar strength.

Despite the tightening in market conditions, the Fed has made it clear that growth needs to slow to achieve its inflation goal of 2%. It will keep rates high and restrictive into at least mid-2024.

As Chair Powell recently noted: “Reducing inflation is likely to require a period of below-trend growth and some softening of labor market conditions.”

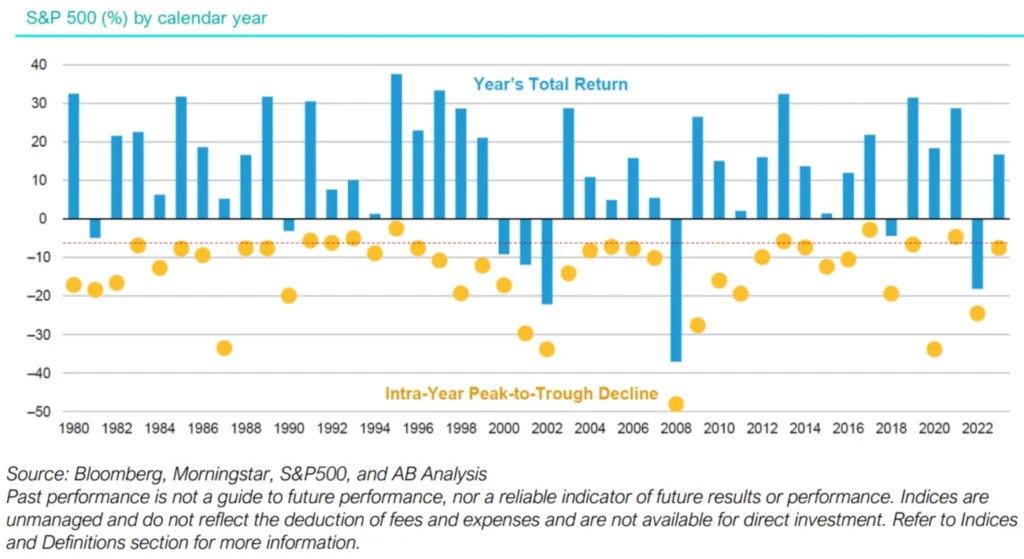

Positioning: Market corrections are normal and can bring opportunity.

Markets typically correct once or twice each year, but the majority of the time even notable corrections still resulted in a positive overall yearly gain.

Historically, corrections are healthy. They reset valuations, remove froth in the markets, and provide opportunities. We can see such opportunities emerging from this corrective action in our Stability and Diversified exposures.

Stability:

The recent rise in longer-dated US Treasury yields provides an opportunity to lock in ~5% returns for 10 years. We have not seen this kind of seemingly relatively risk-free opportunity in decades. If we are right that the Fed can reduce inflation and ease next year, locking in such yields will avoid the reinvestment risk of holding shorter-term assets.

Exposure to long-dated US government bonds serves as portfolio ballast if growth disappoints more than expected. In this sense, longer-duration bonds provide a degree of recession protection, paying us for the added risk of a longer maturity.

Diversified:

As rates have risen, the return opportunity for credit has also risen. Part of the potentially outsized return available in credit today is a function of the higher cost of capital and part is a function of the turmoil in the banking sector. Banks are facing higher costs of funding for deposits and now need to shore up balance sheets in the face of increases in regulatory capital. This has caused them to retrench from riskier business, such as lending to private markets, leading alternative credit providers to fill the gap. Marquee credit platforms are generating low double-digit returns by lending to companies and other investors who need access to funding.

While lending into a slowdown brings risks, we focus on lending opportunities to profitable companies high up in the capital structure (senior secured, first lien) or asset backed with significant levels of collateral, as strong asset coverage and profitability can cushion risks in an economic slowdown. We are looking to combine this attractive absolute return opportunity with other diversified asset exposures positioned to provide downside protection.

Growth:

While equity markets may remain volatile, it is worth noting that higher Treasury yields do not mean stocks cannot perform. Inflation-adjusted yields averaged 3.5% between 1985 and 2005 (well above the current 2%) and yet the S&P 500 annualized at 15% per year.

We remain well diversified in terms of geography, sector, and style and are focused on quality assets. Quality companies with little or no leverage are in the best position to weather an economic slowdown. In June we added to quality mid-cap and value in the US, sectors that had underperformed in the early year rally and trade at multi-decade discounts relative to both their own history and large caps. Mid-caps have outperformed in most decades over the past century.

Outlook to 2024: An improving picture.

Our base case is that inflation grinds lower as the US economy slows and that the Fed achieves that ever-elusive soft landing, defined as slowing growth without considerable damage to the economy and serious damage to the labor market. Soft landings are unusual and have happened just twice since 1970 (after the 1984 and 1994-95 tightening cycles) and might also have happened after the 2015-18 cycle in the absence of the pandemic.

What we know about soft landings:

- Once the tightening cycle was over, the stock market accelerated quite rapidly.

- Innovative technologies and enthusiasm around innovation growth and investment spend accelerated the advance.

Of course, steering the world’s largest economy into a soft landing as the rest of the world slows is not without significant risk. We, like the rest of investors, will be focused on economic and earnings data ahead to confirm or adjust our positioning.

One historical fact is also worth noting. We have never entered a recession in an election year in data going back to 1945. This may be partly due to the tendency of the Fed to raise rates in the pre-election year, so that high rates do not become a political issue.

In summary:

Diversification across asset classes is helping us weather the current volatility, while the rise in yields brings opportunities to our Stability and Diversified exposures. We think that public and private markets are poised to benefit once the tightening cycle has abated. Growth assets in quality companies with a significant valuation cushion and assets exposed to long-term secular trends such as in Generative AI and the climate transition should perform better as we move into 2024. See our recent pieces for further insight.

On a final note, our hearts and prayers are extended to those impacted by the terrible events in Israel.

While the human scale and tragedy is terrible, so far it has had limited impact on markets. US government bond prices and the US dollar have strengthened somewhat. Oil prices have risen to above $90. A broadening of the conflict would change the equation, however.

From a policy perspective, Hamas’s surprise attack may diminish the ability of President Biden to shape a deal that normalises relations between Saudi Arabia and Israel. A diplomatic solution is desperately needed, though as we write no clear end of the conflict is in sight.

A truly devastating series of events for hopes of greater peace in the region.

Download the PDF version of our commentary below.

About the Author