How Global Infrastructure Transformation is Influencing the Investment Landscape

By Alex Hokanson

Deglobalization, decarbonization, and digitization are driving increasingly exciting investment opportunities in infrastructure. Technological advancement in areas such as Generative AI (Gen AI) and digital communications, and public-policy initiatives through the Inflation Reduction Act and Chips Act, are driving significant private-sector and public-sector capital into critical infrastructure. Opportunities for return abound. But significant scale and operational expertise are essential to make the most of the opportunity says Alex Hokanson.

Infrastructure makes the world go round. From the physical systems we have long taken for granted – transport and energy, for example – to the digital networks we have come to depend on, society cannot function without it. And the investment case for this asset class looks increasingly convincing too.

Most obviously of all, exposure to infrastructure offers investors an opportunity for portfolio diversification. A combination of yield – often with inflation protection built in – and capital gains has enabled private infrastructure to match the total returns delivered by global stock markets over the past 15 years. And those returns have come with far less volatility than global equity markets1.

In addition, the correlation between returns from infrastructure and from other asset classes, including equities, is low2. Infrastructure therefore provides investors with a valuable alternative return profile that is beneficial for risk-management purposes.

Moreover, while this return profile is eye-catching at any time, there are good reasons for investors to take a particular interest in infrastructure right now. As the widely followed Chairman and CEO of BlackRock, Laurence D. Fink, recently put it:

“Infrastructure is one of the most exciting long-term investment opportunities, as a number of structural shifts re-shape the global economy. We believe the expansion of both physical and digital infrastructure will continue to accelerate, as governments prioritize self-sufficiency and security through increased domestic industrial capacity, energy independence, and onshoring or near-shoring of critical sectors. Policymakers are only just beginning to implement once-in-a-generation financial incentives for new infrastructure technologies and projects.”3

At AlTi, we share Larry Fink’s view. We believe investors in infrastructure could benefit from three extremely powerful global trends:

1. Deglobalization Reshaping the Global Economy

The Covid-19 pandemic and mounting geopolitical tension have forced both states and corporates to rethink growth and industrial strategy in recent years. Businesses dependent on extended international supply chains no longer feel resilient. The race for raw materials and natural resources is fierce. Nationalism and protectionism are on the increase.

Against this backdrop, a wave of onshoring, near shoring, and strategic investment in key industries has emerged. However, this process of deglobalization requires countries to make major new investments in infrastructure, particularly in transport, shipping, and other areas of logistics, to support this domestic reindustrialization. Highways, railways, bridges, tunnels, and ports all need to be upgraded.

The scale of investment required is huge. In 2017, the McKinsey Global Institute estimated that $3.7 trillion would need to be spent every year until 2035 in order to support expected global rates of growth4. Interventions such as the US’s Inflation Reduction Act and Chips Act are already directing significant additional investment into key areas of infrastructure. Private-sector actors, seeing the opportunity for greater resilience and in many cases taking advantage of attractive tax incentives, are also increasing investment spend.

Moreover, this is a continuing story. The decoupling of the US and China is a remarkable phenomenon. As recently as 2018, China accounted for around 22% of US imports, according to the United States Census Bureau; this has now fallen below 15%, with Mexico on the verge of overtaking China5.

As the US and China continue to trade protectionist blows – from China’s bans on exports of rare earth minerals to the US’s recent tariffs on $18 billion of Chinese goods – the pace of deglobalization and protection of national interests will remain high. Biden administration officials said the additional tariffs are there to shield the big domestic investments in industrial manufacturing made under his watch from Chinese competition and supply-chain disruptions. Tariffs will necessitate further investment in the infrastructure required to facilitate a reshaped global economy with very different patterns of trade.

2. Decarbonization Accelerates to Combat Climate Change

The climate-change imperative is driving capital into decarbonization projects all around the world. Renewable energy – wind and solar in particular – accounts for an increasing share of electricity generation. Advances in areas such as energy storage are gathering pace. Transmission grids are being reimagined to enable the delivery of greener energy.

This rush to decarbonize represents an unparalleled investment opportunity. It’s estimated that global investment of close to $3 trillion a year is required to achieve net-zero goals by 2050, according to a report by consultants Wood Mackenzie6. Others put the sum at closer to $7 trillion7. Whatever the investment required, we know spending and investment in the energy transition needs to substantially increase from where we are today.

This type of investment spending is generating opportunities for investors all around the world. More than 140 countries have set net-zero targets, covering about 88% of global emissions, and more than 9,000 companies have joined the United Nations-backed campaign Race to Zero, pledging to take rigorous, immediate action to halve global emissions by 20308.

We see climate technologies and the energy transition as a major investment opportunity for our clients.

3. Digitization Sweeps All Before It

Public-policy initiatives are providing a strong market backdrop for digital infrastructure. Chip War author Chris Miller wrote in the UK Financial Times: “With recent multi-billion-dollar grants to Intel, TSMC, Samsung, and Micron, the US government has now spent over half its $39 billion in Chips Act incentives. In so doing, it has driven an unexpected investment boom. Chip companies and supply-chain partners have announced investments totaling $327 billion over the next 10 years, according to Semiconductor Industry Association calculations. US statistics show a stunning 15-fold increase in construction of manufacturing facilities for computing and electronics devices.”9

Many organizations believe its future now depends on digital transformation . That will require ongoing investment in a range of digital infrastructure, from the fiber and cell-tower networks that support connectivity to the data centers that deliver cloud-computing capacity.

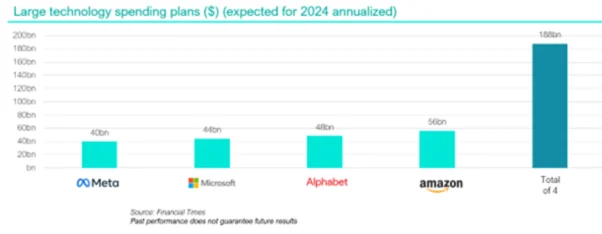

Leading technology companies have already made their plans clear, with the capital expenditure by Alphabet, Amazon, Microsoft, and Meta alone this year to total about $188 billion, almost 40% more than in 2023. They are conservatively expected to spend a further $200 billion in 2025. Few other companies in the world have the cash on hand to credibly embark on this type of capex program, aimed at extending their competitive advantage in Gen AI.10

Infrastructure demand from companies and other organizations will remain huge. We believe they regard moving to the cloud and outsourcing their IT infrastructure as essential if they are to take full advantage of tools such as data analytics, machine learning, and artificial intelligence (AI). The global data-center market is therefore booming, particularly at the hyperscale end – a recent Precedence Research study11 predicted it would expand at a rate of 27.9% per year between 2022 and 2032.

The explosion of interest in Gen AI has only strengthened this trend. The Synergy Research Group thinks the total capacity of global hyperscale data centers will almost triple over the next six years in order to meet the needs of Gen AI12. Significant new capacity is required to train the large language models on which the rapidly maturing technology depends.

But Gen AI needs power!

Goldman Sachs estimates that data-center power demand will grow 160% by 2030. Data centers will use 8% of US power by 2030, compared with 3% in 2022. US utilities will need to invest around $50 billion in new generation capacity just to support data centers alone. This is not just a US phenomenon. Europe has the oldest power grid in the world, so keeping new data centers electrified will require more investment.13 Goldman analysts expect nearly €800 billion in spending on transmission and distribution over the coming decade, as well as nearly €850 billion in investment on solar, onshore wind, and offshore wind energy14.

AI is triggering a wave of investment in power capacity. Brookfield, one of our infrastructure managers, is developing a $10 billion renewable-electricity project, backed by Microsoft, in a deal that underscores the race to meet clean-energy commitments while satisfying the voracious energy demand of AI. This announcement will aim to provide more than 10.5 GW of power delivered over five years backed by power purchase agreements (PPAs). It is almost eight times larger than the largest single corporate PPA ever signed. Microsoft has committed to ensuring 100% of its electricity consumption is “matched” 100% of the time by “zero-carbon energy purchases” by 2030, using mechanisms including these power purchase agreements and renewable energy-certificates15. We believe some of the most interesting investment opportunities lie at the intersection of Gen AI and power.

We’ve also seen strategic relationships from infrastructure investors, renewable developers, and data-center operators. For example, Blackstone Infrastructure Partners has invested nearly $4 billion of equity capital in Invenergy, one of the largest renewable developers in the US16. Blackstone also owns QTS, one of the largest and fastest-growing data-center operators17. These are the types of investment opportunities we seek exposure to.

Taking Advantage of the Opportunities

The infrastructure opportunities are exciting, but it’s important to secure exposure to them in the right way – through vehicles managed by investors with expertise and experience in the asset class. Infrastructure can be an illiquid asset class with significant execution risk, so diversification and professional management are crucial.

Our approach at AlTi is to work with leading infrastructure groups with consistent track records of strong long-term performance. We look for asset managers and other groups that provide diversified exposure to the most attractive assets. Our own experience in climate-focused investment is also important; indeed, there are multiple opportunities for investors interested in infrastructure that aligns with decarbonization objectives.

For many investors, infrastructure is now a compelling asset class with the potential to provide something different. It sits comfortably alongside assets such as equities, offering diversification benefits as well as the potential to deliver tax-efficient, stable, and competitive returns over the long term, with the added benefit of inflation protection and low correlation to other asset classes.

This is why we are so excited about this asset class.