Market Snapshot | February 2026

By Nancy Curtin

Markets and Investments

By Teresa Wells Published October 16, 2023

The asset management industry is a crucial, vibrant force in our economy because it allocates trillions of dollars to businesses in every sector and determines opportunities for wealth creation for individuals, enterprises, and entire communities. In addition, the asset management industry provides a pathway for successful asset managers to create wealth for themselves.

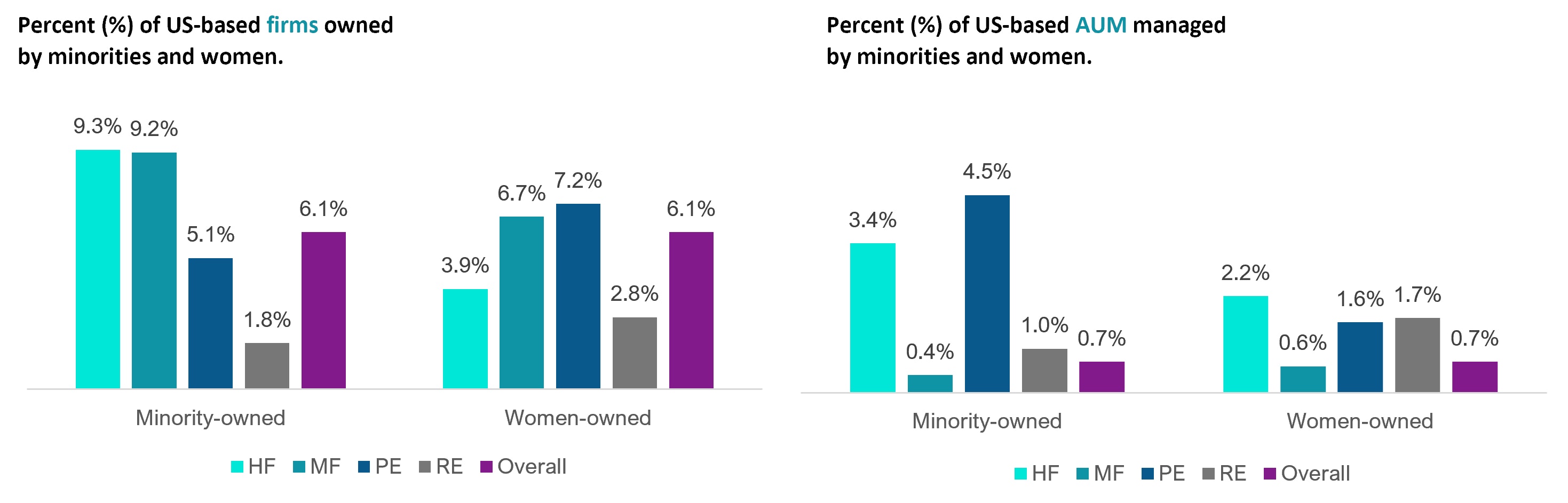

However, lack of diversity within the asset management industry today prevents that prosperity and influence from flowing equitably. A recent study by the Knight Foundation finds that women and people of color own 12.2% of US-based asset management firms, but these firms manage only 1.4% of total U.S.-based AUM.1 In other words, 98.6% of all assets managed in the United States are managed by firms owned by white men.

Over the past few years there has been a greater push to examine the systemic barriers in the asset management industry and to act decisively to create a more inclusive financial system. For example, the 2020 Belonging Pledge invited investors to have internal discussions about what’s needed to advance the practice of investing with a racial equity lens. Similarly, Due Diligence 2.0 provided concrete actions that asset allocators could take to reduce inherent bias when evaluating underrepresented fund managers.

Guided by those frameworks, we reflected on our own practices and assumptions. Regarding AUM for a first-time fund, how small is too small? When assessing a manager’s ability to make good investments, what type of experience is most relevant to future success? Those types of questions pushed us to find areas where we could maintain our investment discipline while evolving our diligence process to widen the net and keep great, often-overlooked managers in our pipeline.

As a result, we developed within our impact investing practice the Emerging Manager focus, which seeks to deliver more capital to the next generation of fund managers who better reflect our society. While the initiative supports early managers broadly, we emphasize bringing on managers from historically overlooked backgrounds, including women and people of color. We bring our usual rigor, while leaning on an expansive due diligence toolkit developed to evaluate younger organizations and investment strategies with limited track records. For every Emerging Manager selected, the core elements for success are there: a compelling investment thesis, relevant experience, and strong team and networks.

These efforts have already borne fruit. We have increased our exposure to an innovative and exciting set of investment strategies that would otherwise have been missed. We have also meaningfully increased the number of approved asset management firms owned and led by women and people of color, bringing us well above industry averages.

We continue grappling with the questions, and still have work to do to make our investment platform more inclusive. But our experience thus far has deepened our learning. Below, we share some key insights:

Leading with relationships. Launching a first-time fund is extremely difficult and courageous. It is no small feat to start an investment business from scratch, especially without the benefit of institutional backing, meaningful start-up capital from friends and family, or other connections or tailwinds others enjoy. Emerging managers, therefore, do not always have every administrative element buttoned up. But those gaps do not have to squelch our engagement with the managers. Instead, recognizing our positional power, we have identified opportunities for trust-based collaboration. For example, when invited, we have helped negotiate licensing relationships, edit client forms, formalize policies and procedures, and make connections to auditors, administrators, and lawyers. Even in the instances when we do not provide financial investment, this approach has enabled us to form strong relationships in support of underrepresented managers.

Assessing value drivers more holistically. For years, standard practice has been to rely primarily on the manager’s track record of investing to determine a strategy’s risk or value. However, professional, academic, and lived experiences all contribute to a manager’s ability to make investment decisions. Especially with impact solutions, where we are seeking more than just capital returns, we have seen how managers can draw from many dimensions of their background to create value.

Yes, we want managers who know how to invest capital. We have simply seen ample evidence that experiences outside the typical pedigree can enhance that ability. Conversely, highly experienced traditional investors who do not share connectivity to the constituencies they aim to serve can be a material risk if they make faulty assumptions or ill-advised missteps that drive unintended outcomes.

Although seeking managers with specialized backgrounds has always been a part of our due diligence practice, for emerging managers especially, we have deepened that practice in two key ways:

Committing senior internal resources. It can be a tall order to ask an early-career analyst to evaluate an emerging manager. There is too much career risk involved in championing a strategy that may not resemble others already on the platform. The standard quantitative and peer group-based tools junior analysts are trained to apply in the analysis of an investment fund may be less useful in this situation. This means that most junior analysts would likely be inclined to pass early on a potential investment with an emerging manager. This is why we at AlTi dedicate more experienced senior members of the investment team to take the lead on meeting with and analyzing emerging managers. The credibility of their past work allows them more freedom to explore and be creative, enabling more context-appropriate evaluation and support of emerging managers. Through close collaboration in the process, our junior analysts gain mentorship and training on how to evaluate emerging managers. This organizational approach demonstrates to the investment team, the firm, and external partners that we are committed to this work.

Viewing fees with nuance. Asset management is a business. First-time emerging managers earn revenue by charging investors a fee to invest on their behalf. In time, these managers will earn additional revenues as they participate in the profits of their investments. But the management fees they earn initially are their way to pay salaries and keep the lights on. As mentioned earlier, many underrepresented managers do not have access to financial resources (i.e., friends and family, personal wealth, etc.) to subsidize the management fees and keep the business solvent. Thus, we have had to grow more comfortable with this fact: to truly and sustainably drive more diversity within this field, in some cases, the management fees might be on the high side – at least initially. Of course, we are a business, too, and we seek to act in the best interests of clients. But keeping our longer-term goals in mind, we have worked with high-potential managers to understand their business financials and reconcile what they need to charge in fees to make their business manageable.

Determining what kind of capital is best. Most of the issues we face today are complex, requiring a multifaceted response. We reject the notion that every solution should either drive a ‘market rate’ of return or be consigned to philanthropy. Instead, we think across a full continuum of capital – from philanthropy to catalytic capital to blended finance to market rate. We spend considerable time researching and evaluating not only how money flows through a particular investment, but how that capital influences all stakeholders in the system, and whether it is the right kind of capital to drive the best impact outcomes. For instance, to support diverse entrepreneurship, one might consider low-interest loans to community-led CDFIs to fund lower-growth small businesses, as well as a venture capital strategy supporting BIPOC tech entrepreneurs. Either form of capital can work for the right kind of businesses. For that reason, we support emerging managers across the capital continuum from all asset classes – VC and private equity to CDFIs and community loan funds.

Through this work, we and our clients have been opened to a growing field of emerging managers and strategies – opportunities for compelling returns and heightened impact that we would have missed if we continued to do things the same ol’ way.

While we have benefitted from years of researching impact and emerging managers, we are excited by the continual evolution of the field and our commensurate learning journey alongside it. For example, we are looking to widen our scope to include more groups who have faced similar challenges of marginalization, including people who identify as LGBTQIA+, people who are differently abled, people living in rural communities, and others. Through field-based research, detailed theory of change work, and constant reflection on our research methods, we aim to do our part to continue advancing a more equitable financial and economic system.

Sources: 1/ https://knightfoundation.org/reports/knight-diversity-of-asset-managers-research-series-industry/

_______________________

About the authors:

Antonio Casal

Antonio is a senior member of AlTi’s Investment Group. He leads the manager research team and oversees manager research for traditional and impact investments across all asset classes. His responsibilities include sourcing, due diligence and ongoing monitoring of money managers.

Donovan Ervin

Donovan (he/him) is a member of AlTi’s Investment Group, where he is helping to direct capital toward a more inclusive, just, and regenerative economy. Previously, Donovan has held positions at various organizations in the social sector, including from K-12 education, community development, and environmental justice.

Teresa Wells

Teresa Wells is Managing Director of U.S. Wealth Management at AlTi. She is a frequent speaker, writer and moderator and is widely regarded as an expert on issues of gender equality and inclusion in the fields of finance and investing.

Teresa Wells is Managing Director of U.S. Wealth Management at AlTi. She is a frequent speaker, writer and moderator and is widely regarded as an expert on issues of gender equality and inclusion in the fields of finance and investing.

Notes & Important Disclosures

This information is being provided by AlTi Global, Inc. (“AlTi”), exclusively for use by recipient. For the purposes of this disclosure, AlTi includes certain of AlTi’s affiliates that are registered as investment advisers with the U.S. Securities and Exchange Commission, (each, an “AlTi Affiliate RIA” and collectively, “AlTi Affiliate RIAs”) that provide investment advisory services. Any investment products referred to herein are managed and / or advised by one or more of AlTi Affiliate RIAs. No part of this material may, without AlTi’s prior written consent, be copied, photocopied, or duplicated in any form, by any means. AlTi is providing this information solely in connection with providing general investment advisory services and is not in connection offering investment advisory services with respect to any “private funds” that are managed by such AlTi Affiliate RIAs. The information provided is in no way intended to be considered a recommendation, or an offer to sell, or a solicitation of any offer to buy, an interest in any security, by AlTi or any AlTi Affiliate RIA, including an interest in any investment vehicle or any other financial product, including any investment advisory, wealth planning or trust arrangement managed or advised by AlTi or any AlTi Affiliate RIA, nor does it constitute investment, legal, or tax advice with respect to the products and services and it is important that you do not rely on its content when making an investment decision. Neither AlTi nor any AlTi Affiliate RIA make any representations through this information as to whether any security or other financial product is suitable to you or will be profitable. This information is not intended as a formal research report and should not be relied upon as a basis for making an investment decision. You should obtain relevant and specific professional advice before making any decision to enter into an investment transaction. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investments are not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other governmental agency. Prospectuses and offering documents should be read thoroughly before investing. No representation is made that any client will or is likely to achieve its objectives, that the strategies, investment process or risk management referenced in the information provided will be successful, or that any client will, or is likely to, make any profit, or will not suffer losses, including loss of principal. Past performance is no guarantee of future results. Opinions regarding the suitability of investment approaches, including risk allocations and other portfolio decisions, are not tailored to any specific client, do not constitute recommendations, and are solely provided to facilitate discussion. Individual investor portfolios are constructed based on the individual’s financial resources, investment goals, risk tolerance, investment time horizon, tax situation and other relevant factors. Any statements, assertions or the like (collectively, “Statements”) regarding prior or future market or other events, or views about investing, are based upon AlTi’s beliefs, which may not reflect those of the firm as a whole, unless the information provided includes the source(s) with respect to such Statements. Additionally, AlTi Affiliate RIAs may pursue investment strategies for clients that do not reflect or contradict the beliefs set forth in any Statement at any time, including at the time of publication. The Statements involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond the control of AlTi. Future evidence and actual results could differ materially from those set forth in, contemplated by, or underlying these Statements, which reflect AlTi’s beliefs at the time of publication and are subject to change. In light of these risks and uncertainties, there can be no assurance that these statements will prove to be accurate in any way. Information given herein is believed to be reliable, but AlTi does not warrant to its completeness or accuracy, nor does AlTi assume any obligation to update or revise such information. Certain information has been provided by and/or is based on third-party sources and, although believed to be reliable, has not been independently verified and AlTi is not responsible for third-party errors.