Catalyzing Impact with Community Development Financial Institutions

By Donovan Ervin

Limited Capital for High-Impact Companies

High-impact businesses need capital that matches their structure, timeline, and reality.

Consider this: A woman- and Native-owned farming company in the Pacific Northwest, we’ll call it Project Seed Bank, aims to feed tribal neighbors, steward the land, and promote economic development. Project Seed Bank employs regenerative, biodynamic Native farming practices to grow Native crops – such as tribal peppers, tomatoes, herbs, and flowers – for Native communities, while also offering a line of packaged tribal sauces, teas, and snacks. The founder-owner, like any business leader, needs financing to make strategic purchases for business stability and growth.

However, conventional finance doesn’t meet the needs of this type of business. Because of historical discrimination and ongoing disinvestment, many traditional lenders don’t operate in rural and Native communities.1 Even if Project Seed Bank were to qualify for a traditional loan, the lender would charge a high interest rate and require collateralization of personal assets, on account of higher perceived risks. Moreover, repayment of the loan would likely begin immediately, despite the seasonality and prolonged harvesting and sales cycle of a food production business. Traditional capital, therefore, can lead to a relentless cycle of debt that can destroy the business and deepen mistrust of the financial industry, all to the detriment of the community.

Catalytic Capital to Fill Gaps in Capital Markets

Fortunately, catalytic capital is a type of impact investment that intentionally aims to fill these financing gaps. Acknowledging the limitations of conventional finance, catalytic investors accept lower risk-adjusted financial returns in exchange for greater social or environmental impact.

In the case of Project Seed Bank, a Native-led Community Development Financial Institution (CDFI) provides low-interest, patient, and culturally responsive loans that meet the distinctive needs of Native-led food businesses. One of the loan products offered, for example, charges a significantly lower interest rate and allows borrowers to make interest-only payments for up to five years before beginning principal repayment. The CDFI also provides technical assistance to help borrowers enhance their business operations. In this financing model, producers are given a fair chance to employ indigenous, ecologically sound production methods, provide food for their communities, and grow a prosperous enterprise.

More broadly, this approach to catalytic investing can propel transformative societal outcomes. Without the pressure to quickly deliver profit-maximizing returns to investors, capital providers like CDFIs are empowered to offer financial tools that better address the nuanced needs of the intended beneficiaries. Moreover, when investors accept lower financial returns, catalytic providers can, in turn, charge lower rates to end borrowers. This helps to keep capital circulating in target communities, which can accelerate economic development and enhance overall impact. In fact, recent research from the Miller Center for Global Impact estimates that intentional catalytic investment can multiply impact by 6x – 40x.2

CDFIs as a Key Feature of Catalytic Investing CDFIs are catalytic by design. For context, CDFIs are certified organizations offering financial products tailored to the specific needs of low-wealth, communities that are underserved by traditional finance.

Nationwide, in rural and urban areas and Red and Blue states, there are over 1,400 designated CDFI entities listed as community development banks, credit unions, loan funds, and venture capital funds. Some have a national footprint, while others are regional or local. CDFIs provide a wide range of products, including FDIC-covered personal checking accounts and Certificates of Deposits, individual and small business loans, and larger loans supporting community organizations.

And they operate in high-impact themes and sectors, including affordable housing, education, healthcare, small business lending, energy efficiency, and, as noted above, Native food production. In addition to providing financial capital, many have robust technical assistance programs, financial education training, and policy and research arms.

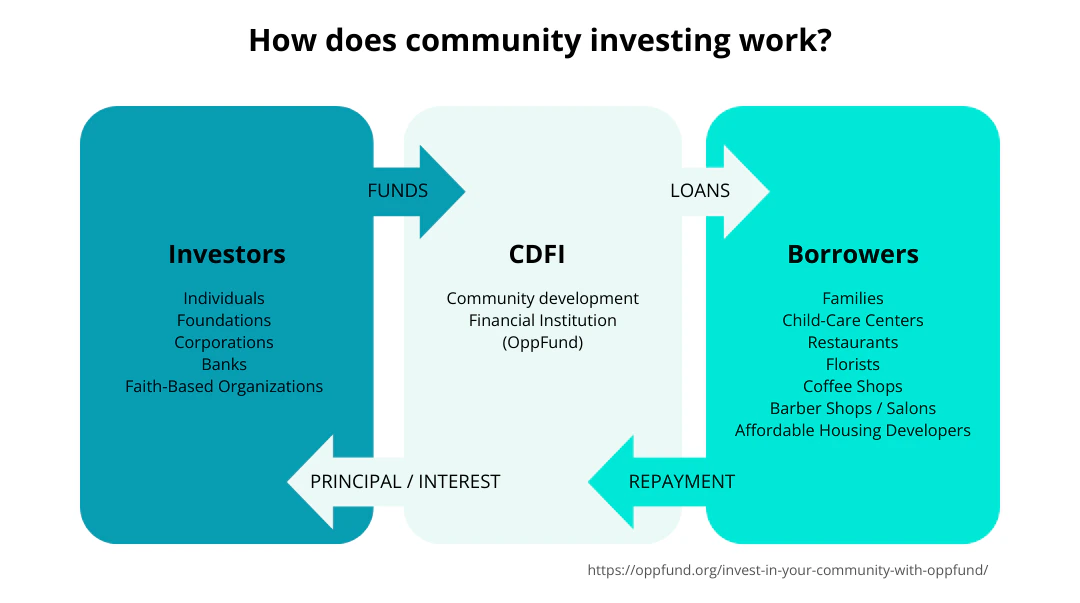

How community investing works

As catalytic intermediaries, CDFIs source capital from external investors and redeploy that capital to community borrowers. Notes programs provide a critical source of capital for community investing. An investor makes a loan to a CDFI, typically at a rate of return lower than an investor could get from comparable investment opportunities. The CDFI then offers high-impact, affordable loans, along with hands-on support, to the end borrower. The revenue from those community loans covers note repayment and some CDFI operations.

This type of investing is critical for companies like Project Seed Bank, but it comes at a financial cost to investors. The model only works when catalytic investors acknowledge structural barriers and are willing to accept lower financial returns in exchange for deep impact. Even still, most CDFIs employ an integrated capital approach, meaning they use grant funding in addition to interest income to achieve their mission.

CDFIs as Viable Investments

Although they don’t address every gap in impact capital markets, CDFIs tend to be core components of catalytic investment portfolios because, as outlined below, they are well equipped to deploy patient, community-centered capital at scale.

- High impact & additionality – Roughly two-thirds of CDFIs cannot fully meet the demand for their products,[1] indicating that CDFIs are filling a significant need that would otherwise go unmet.

- Historical financial performance – Thanks to rigorous underwriting and risk management, CDFIs have had a historical loan loss rate of less than 2%, which is on par with bank loans.[2] This enables confident allocations.

- Well-established, regulated industry – The CDFI Fund, a bipartisan-supported entity within the US Department of Treasury, certifies CDFIs and administers federal grants to CDFIs. This regulatory oversight, in conjunction with industry groups and ratings agencies, promotes transparency.

- Aligned with investor interest – The wide range of sectors and geographies covered by CDFIs offer pathways to more efficiently allocate catalytic capital according to investors’ theories of change.

AlTi’s Approach to CDFIs

At AlTi, CDFIs are an important component of our catalytic impact investment platform. We have partnered with several national and regional CDFIs, typically allocating to promissory notes programs. As with all investments on our impact platform, we perform rigorous due diligence, assessing key factors for success, including team, strategy, portfolio performance, and organizational sustainability. Given the intentions of our catalytic program, we hold these groups to the highest standard of impact by closely evaluating criteria such as intentionality, additionality, outcomes, and proximate leadership.

CDFIs Facing Macro Threats

Despite their strong impact, performance, and support, CDFIs have recently encountered macro challenges.

In 2025, funding for the CDFI Fund was suspended by executive order and the government shutdown. Bipartisan advocacy enabled the CDFI Fund to resume certifying CDFIs and distributing federal grants as quickly as feasible, demonstrating the industry’s resilience. However, these interruptions have taken a toll on the sector by forcing CDFI leadership to spend more time defensively planning for instability, instead of focusing on deploying capital to communities.

Other exogenous factors threaten CDFIs. For example, if federal government stops enforcing the Community Reinvestment Act (CRA), CDFIs may see less philanthropic and investment capital from larger private financial institutions. Additionally, broader economic volatility could trigger higher default rates among vulnerable borrowers, while simultaneously increasing the need for CDFI financing.

A Critical Opportunity

At a moment when capital gaps are widening and macro headwinds persist, catalytic investors have a meaningful opportunity to strengthen the CDFI ecosystem in the following ways:

- Invest: support the investment activities of CDFIs by providing them with low-cost capital.

- Give: make a philanthropic grant to a CDFI to support hands-on services and overall operations.

- Advocate: communicate your support for CDFIs to family, friends, colleagues, and policymakers.

About the Author