Alternative Proteins: Are they worth the investment?

By AlTi Global

The term alternative protein has become synonymous with alternatives to meat, but there are also lesser known but growing markets in alternative fish, fat and dairy products and the technologies that propel them. Increased awareness of the negative impact of consumer behaviour on our environment, a focus on health, advancements in technology and, more recently, the Covid-19 pandemic have all played a part in the recent surge of interest in the “Alternative Protein” space. But what exactly is alternative protein, and will it really be a viable substitute for the future?

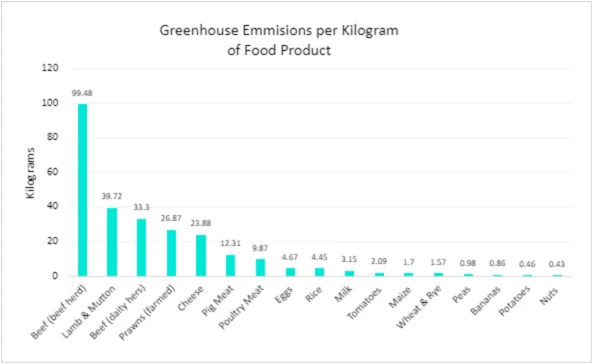

Food production and consumption make up more than 20% of global greenhouse emissions and 15% of that comes from livestock; bovine meat is the greatest culprit having the least efficient calorie conversion ratio from feed input and subsequent food output.1

Greenhouse emmisions per kilogram of food product2

Source: Our World in Data, October 2019

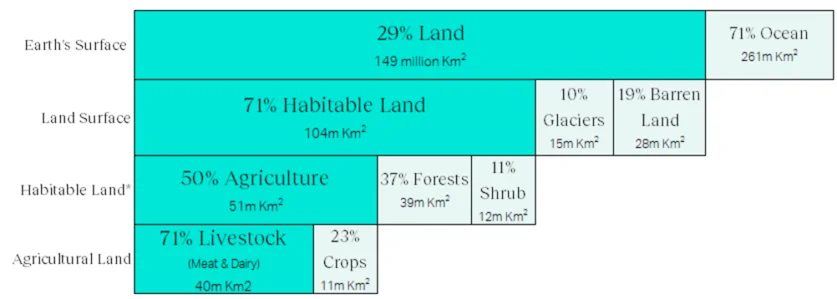

Concurrently, there is a significant strain on land available to produce food. While global farmland for livestock makes up 77% of the total, that livestock represents only 18% of global human calorie intake, making for an inefficient use of a finite resource.3

Global land use for food production4

*The balance is 1% Urban & built up land; 1% Freshwater

Source: Our World in Data, November 2019

Today consumers are also looking for healthier alternatives to their more traditional diets, which typically includes less red meat and more “conscious” consumption. This has given rise to a generation on “flexitarians”; 1 in 3 people in the UK already identify as flexitarian.5

Simple plant-based proteins (e.g., soy and bean-based) despite being the most established have struggled to grow greater market share due to their perception as inferior substitutes. Fermented protein processes are also nothing new in the world of alternative food production, examples include beer, yogurt and cheese (traditional), and Quorn (biomass).

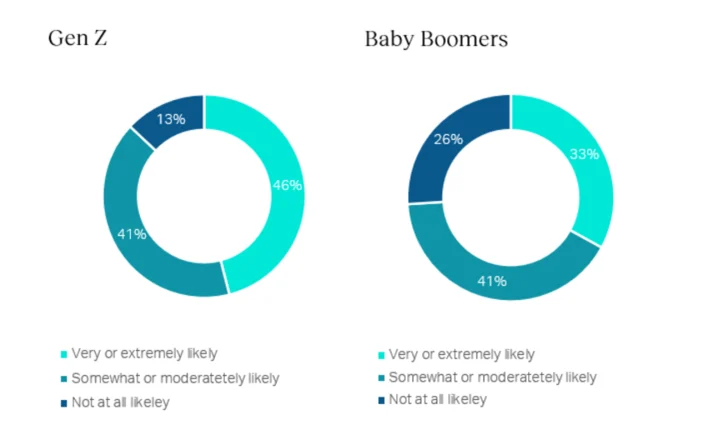

Openness to trying cultivated meat by generation

Cultivated (cultured) protein products are more nascent but appear to be gaining greater traction. There are clear benefits: specifically, the process removes the need for traditional methods of meat production, and so requires less energy and leads to lower emissions. But this is a costly process, not sufficiently proven and is hard to scale given the time it can take to create cell lines, and costs to reaching commercial viability.6 The technology is strong but nascent, and still evolving with few commercial examples today.

Singapore was the first country to approve a cultivated meat product from US-based Eat Just, as recently as 2020.7 The FDA meanwhile only approved its first “chicken” product in mid-November 2022 and, though approved from a safety standpoint, is yet to be fully approved for sale.8 To put this into context, more than 100 companies have been founded since 2012 to focus on the development of cultivated proteins.9

These events show tremendous progress, but at a glacial pace. Issues with regulation will continue to plague such a nascent industry as the regulation itself is being created alongside the technology meaning companies are operating blind as to how and when products will make it to market, if ever.

Although consumer adoption is slow, it should always be viewed in a generational context: multiple studies indicate that younger consumers are far more willing to try alternative proteins, meaning that a gradual shift in the right direction is already naturally occurring.10

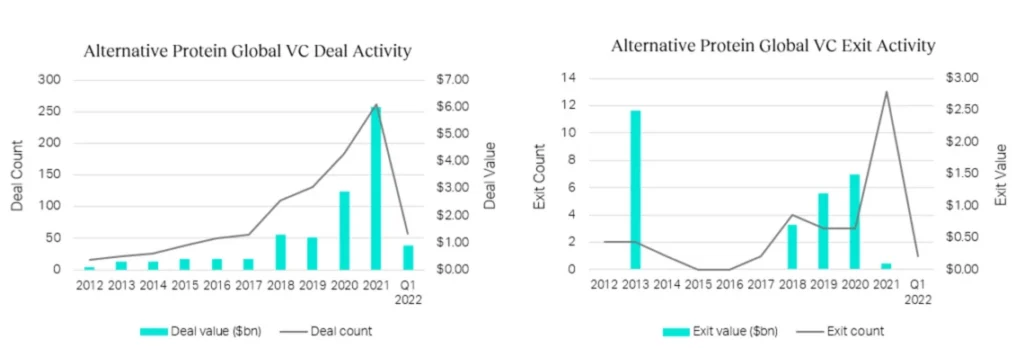

Further investment is key: recent commercial developments were made possible by a wave of recent funding, especially from private markets. It’s often said the Covid-19 pandemic accelerated technological progress across industries, and food and agricultural production was no exception as traditional meat production processes ceased and shortages emerged during lockdown restrictions. This allowed for the alternative options to gain traction as consumers were left with no alternative but the “alternatives”.

Crucially, this shone a spotlight on the alternative protein space and gave start-ups an opportunity to capitalise on the huge amount of liquidity flowing through the market over that period, allowing them to scale in a meaningful way. For example, an early frontrunner Impossible Foods raised more than $2bn since inception just 11 years ago.11

Alternative Protein Global VC Deal and Exit Activity

Source: Pitchbook, Alt-Protein Industry Advances Despite Costs and Red Tape, July 2022

While it’s true that 2020 and 2021 showed an exceptionally strong year-on-year increases in capital raised for companies making developments in his space, 2022 looks set to be disappointing by comparison, reflecting the reliance that an emerging tech industry such as this has on the macroeconomic climate and private investors. It’s clear from the data that exits ground to a halt in the first quarter of 2022 and are not expected to show a marked improvement in in the second half of 2022. Although discouraging, it’s not surprising given the macroeconomic backdrop and is replicated across multiple industries.

As we have demonstrated throughout this piece, this is a complex and continuously evolving segment of a vast market. Not only are the products and methods for production multi-faceted, but the motivations of the consumers they are serving are also extremely complex, and the regulations to allow them yet another known unknown. The macroeconomic headwinds today add a further layer of complexity.

There is no doubt that the alternative protein market will (continue to) disrupt in a significant way going forward, but who, how and to what extent is not yet clear. Ernst and Young estimate that the alternative meat market alone may have more than 40% of market share by 2040, and 60% for alternative dairy.12 McKinsey predicts that if consumer adoption strengthens, by 2030, the cultivated meat market alone could be worth $25bn.13 These are big numbers and represent huge market opportunity, which is why we are continuing to track this segment so closely.

Science, technologies, funding and consumer uptake are all moving in the right direction, but setbacks such as a drop off in funding through 2022 and weak public markets can hamper short term progress, while higher inflation put increased pressure on consumer spending patterns can have a detrimental impact on adoption.

We believe there are some truly exceptional companies out there today and many more not yet in existence that will come to dominate in their focus areas. Those who have already achieved some level of commercial success will likely continue to hold a position of dominance in the market but as technologies advance, they will come under pressure from upstarts. All of this creates an exciting and highly competitive landscape that will present plenty of opportunities for the patient investor.